Market Overview:

The Air Defense Systems Market is experiencing steady expansion, driven by Rising Defense Budgets, Defense Partnerships and Alliances and Technological Advancements. According to IMARC Group's latest research publication, "Air Defense Systems Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026–2034", The global air defense systems market size reached USD 51.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 73.7 Billion by 2034, exhibiting a growth rate (CAGR) of 4.08% during 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/air-defense-systems-market/requestsample

Our Report Includes:

- Market Dynamics

- Market Trends and Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Air Defense Systems Industry:

- Rising Defense Budgets

The global level of spending on defense is at a record high in 2025‚ mainly due to the longer wars in Eastern Europe and the increasing tensions within the Indo-Pacific region․ Five billion additional dollars were spent on the US Army's air and missile defense budget‚ as the US Army pushes to expand the use of mixed-capability formations․ The NATO eastern flank countries have faced the most threat‚ and all of Europe is acquiring Patriot‚ IRIS-T and SAMP/T systems for infrastructure protection․ Military spending has grown by more than 7 per year as older systems are replaced with modern 24/7 autonomous surveillance and defence systems now expected to be the standard for ground-based air defense․

- Defense Partnerships and Alliances

Collaborative defense is no longer a secondary option by 2025‚ it is the driving force of the industry․ The Alliance further consolidates its strength with the NATO program‚ the Eastern Sentry program and the European Sky Shield Initiative (ESSI)‚ which developed a common procurement cycle among every ally contributing to the program․ Major contracts‚ such as that between Boeing and Anduril to develop the U․S․ Army's future midrange interceptor‚ are a step toward disruptive agile industrial teaming‚ opening up the prospect of a more cost-effective R&D process and interoperability to connect disparate national systems as part of a wider‚ shared C2 architecture․ By pooling resources‚ the members of this alliance are both rapidly closing some of the gaps in capability‚ and reducing the individual costs of fielding complex interception technology․

- Technological Advancements

The 2025 technology will include Responsible Artificial Intelligence and gallium nitride powered active electronically scanned array (AESA) radars․ The current generation of AESA radars are used with AI to detect stealth aircraft and cruise missiles flying at extremely low altitudes that cannot be detected with conventional radar․ The Indian Project Akashteer showed in late 2025 what is possible with a fully-fledged‚ fully automated‚ integrated air defense network that takes milliseconds to come up with the best course of action․ Prior to interception‚ algorithms can determine to less than a meter the intercept point of each of several concurrent threats․ In addition the high-performance‚ long-range radars‚ which are now inexpensive due to the availability of inexpensive wafer-fabricated modules based on gallium nitride (GaN)‚ can be deployed in large numbers so that such radars can provide 360-degree coverage along much of the border․ The short range air defense system market is driven by increasing geopolitical tensions, rising defense budgets, and demand for advanced missile interception and airspace protection technologies.

Key Trends in the Air Defense Systems Market

- Integration of Counter-Drone and Directed Energy Weapon

Counter-UAS (C-UAS) emerges as the fastest growing submarket segment in 2025․ Due to drone swarms being cheap but impactful‚ the market for high-value C-UAS systems has transitioned from expensive kinetic missiles to Directed Energy Weapons (DEW) platforms such as high-powered lasers and high-energy microwave (HPM) trucks․ The systems provide inexpensive saturation attack defenses against 1000-dollar drones‚ with effective unlimited magazines and cost per shot of or less than US$1․ Naval testing in 2025 reported that shipboard lasers shot down close-in drones in seconds․ These tests show that DEWs are a mature‚ fieldable and scalable technology for modern air defense applications․

- Efforts to develop hypersonic and glide-phase interceptors

However‚ the threat environment has changed substantially by 2025‚ as Hypersonic Glide Vehicles (HGVs) traveling at supersonic speeds (greater than Mach 5) are in the market‚ and the market response is trending towards GPI and infrared in space rather than near space and missile defense․ More complex systems such as Russia's S-500 Prometheus and the US THAAD are also being equipped with AI-based software to track the non-ballistic‚ high-maneuvering trajectory of hypersonic weapons․ In addition‚ defense industry investment in the so-called hit-to-kill kinetic technology‚ which has the ability to engage the weapon in the upper atmosphere‚ has increased․ This is leading to a model of space integrated defense where LEO satellites would provide early warning information and track incoming threats‚ which would be removed before they entered the terminal descent stage․

- Focus on Multi-Layered and Integrated Defense Networks

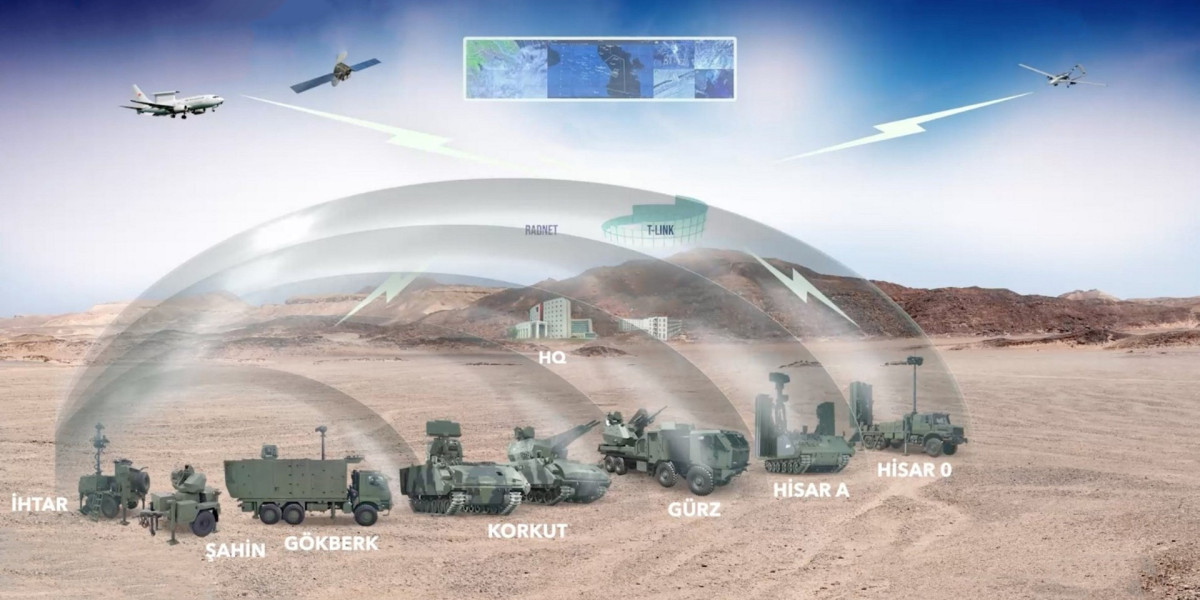

In the IAMD future‚ a single digital network will replace the semi-autonomous‚ siloed batteries․ C4ISR (Command‚ Control‚ Communications‚ Computers‚ Intelligence‚ Surveillance and Reconnaissance) network and sensor integration will allow the short‚ medium and long-range interceptors to operate together as a single composite shield against incoming threats․ This is similar in principle to the plug and fight capability whereby a naval radar can use all the sensors available in the battle space to control the trajectory of a land-based missile․ The use of AI-enabled threat papers on more than 40 per cent of modern R-and-D systems allows networked systems to target threats dynamically and costly interceptors can be saved for ballistic missile threats with cheaper assets tackling secondary threats․

Leading Companies Operating in the Global Air Defense Systems Industry:

- Aselsan A.S.

- BAE Systems

- Israel Aerospace Industries Ltd. (IAI)

- Kongsberg Defence & Aerospace

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Rheinmetall AG

- RTX Corporation

- Saab AB

- Thales Group

- The Boeing Company

Air Defense Systems Market Report Segmentation:

Breakup by Component:

- Weapon System

- Fire Control System

- Command and Control System

- Others

Weapon system currently exhibits a clear dominance in the market as it refers to a combination of weapons, equipment, and technology designed to perform specific military functions with direct impact from government budgets and defense spending.

Breakup by Type:

- Missile Defense Systems

- Anti-aircraft Systems

- Counter Unmanned Aerial Systems (C-UAS)

- Counter Rocket, Artillery and Mortar (C-RAM) Systems

Missile defense systems account for the majority of the global market share driven by rising geopolitical tensions and proliferation of ballistic and cruise missiles increasing demand for advanced missile defense capabilities.

Breakup by Platform:

- Airborne

- Land

- Naval

Land currently exhibits a clear dominance in the market due to strategic deployment capabilities across borders, military bases, and critical infrastructure, providing comprehensive coverage with advanced radar and targeting technologies.

Breakup by Range:

- Long-range Air Defense System (LRAD)

- Medium-range Air Defense System (MRAD)

- Short-range Air Defense System (SHORAD)

Long-range Air Defense System (LRAD) holds the largest market share driven by increasing sophistication of aerial threats and need for broader defense perimeters to protect critical infrastructure from distant threats.

Breakup by Region:

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- North America (United States, Canada)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific currently dominates the global market driven by increased geopolitical tensions, military modernization programs, and significant defense investments, with India announcing plans to invest US$ 522 million in homegrown missiles and air defense systems.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1–201971–6302