Leveraging Professional Assistance

Leveraging Professional Assistance While many companies may manage their reporting internally, seeking professional help can significantly improve the quality and effectiveness of financial reporting. Engaging with financial advisors or accounting firms that specialize in surety bonds can provide expert insights into best practices and reporting standards. These professionals can help in preparing comprehensive reports that meet the expectations of surety companies, ultimately leading to better rates.

Moreover, technology can streamline the bond application process, making it easier for contractors to submit necessary documentation and track their bonding status. By embracing these digital tools, contractors can improve efficiency and make informed decisions regarding their bonding needs.

Is professional assistance necessary for reporting?

While not strictly necessary, professional assistance can enhance the quality of financial reporting. Experts can help ensure accuracy, provide insights on best practices, and prepare comprehensive reports that meet the expectations of surety companies.

How can I improve my chances of getting approved for a surety bond?

Improving your financial health, maintaining organized records, and providing thorough documentation can significantly enhance your chances of getting approved for a surety bond. Engaging with surety professionals for advice and maintaining good credit are also crucial steps.

As projects grow in size and complexity, so do the challenges associated with them. Contractors are often required to present surety bonds to guarantee their performance and compliance with contractual obligations. This requirement adds an additional layer of complexity but also provides opportunities for contractors who understand the nuances of bond management. In essence, construction bonds are not merely a requirement but a strategic tool that can influence a contractor’s reputation and financial stability.

In summary, leveraging professional assistance not only enhances the quality of reporting but also builds a strong foundation for securing favorable surety bond rates through informed decision-making and comprehensive financial insights.

In summary, leveraging professional assistance not only enhances the quality of reporting but also builds a strong foundation for securing favorable surety bond rates through informed decision-making and comprehensive financial insights.Are there different types of surety bonds?

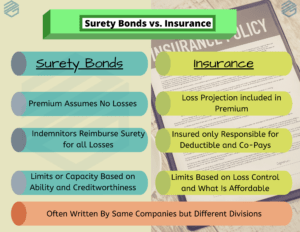

Yes, there are several types of surety bonds, including performance bonds, payment bonds, and bid bonds. Each type serves a different purpose and is required under various circumstances, depending on the type of project or contract.

How do I get a construction bond?

To obtain a construction bond, contractors must apply through a surety company. This process typically involves providing detailed financial information, past project experience, and other relevant documentation to demonstrate reliability and capability.

How can my LLC secure a construction bond?

How can my LLC secure a construction bond?To secure a construction bond, your LLC must prepare and submit various documents, including financial statements, business licenses, project plans, and contracts with subcontractors. Consulting a bonding agent can also facilitate the process by helping identify suitable surety companies.

Aligning Project Timelines with Bonding Needs

Contractors must also align their project timelines with their bonding needs to avoid unnecessary complications. Understanding when a project is expected to commence and the associated bonding requirements allows contractors to apply for bonds at the right moment. This ensures that they are not left scrambling for bonds as project deadlines approach.

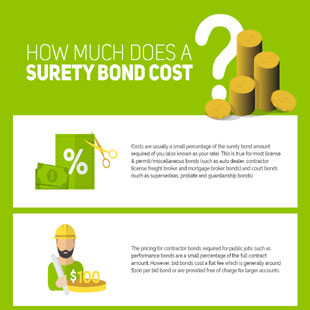

What factors influence surety bond rates?

What factors influence surety bond rates?Factors that influence surety bond rates include the financial stability of the applicant, the experience and reputation of the business, the nature of the project, and the overall market conditions. Each of these elements plays a role in determining the perceived risk associated with issuing a bond.

Another common issue is failing to showcase a company's full potential. Businesses often focus on their most recent accomplishments, neglecting to provide a comprehensive view of their history. This lack of context can make it challenging for sureties to assess the business's overall reliability and risk profile. A well-rounded report should include a detailed history of past projects, challenges faced, and how they were overcome.

Can I apply for multiple bonds at the same time?

Yes, contractors can apply for multiple surety bonds simultaneously. However, it is essential to ensure that each application is well-prepared and meets the requirements of the respective surety companies.

To expand on this point, see the three C’s of surety bonding for a quick breakdown of the essentials. Understanding the timing of bond premiums and the potential cash flow implications can help contractors better manage their finances. By planning ahead and keeping track of the bonding requirements for upcoming projects, contractors can minimize the risks associated with cash flow disruptions during the bonding process.